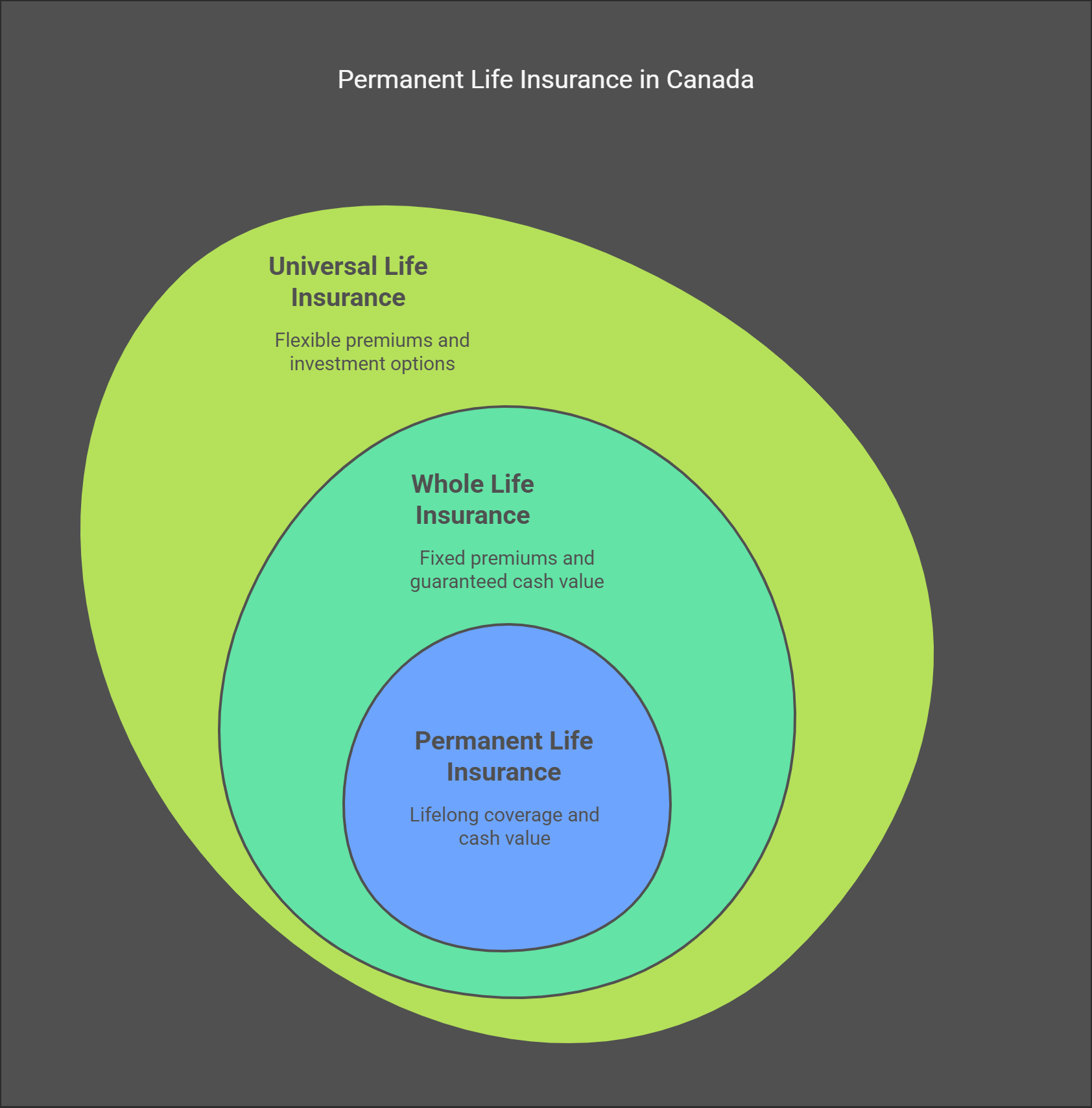

What is Whole Life Insurance?

Whole life insurance is a permanent life insurance policy that provides lifelong coverage and includes a built-in savings component called cash value.

Key Features of Whole Life Insurance

- Guaranteed Death Benefit: Your beneficiaries receive a tax-free lump sum payment upon your passing.

- Fixed Premiums: The premiums remain constant throughout the policy’s life, making it predictable and easy to budget for.

- Cash Value Growth: A portion of your premiums accumulates in a tax-advantaged savings account, growing over time at a guaranteed rate.

- Dividends (For Participating Policies): Some policies pay dividends, which can be reinvested, used to buy additional coverage, or withdrawn as cash.

- Loan and Withdrawal Options: You can borrow against your cash value or withdraw funds (subject to conditions and potential tax implications).

Whole Life Insurance

Advantages:

- Guaranteed premiums and death benefit.

- Predictable cash value growth.

- Can be used as a financial asset.

Drawbacks:

- Higher premiums than term or universal life insurance.

- Less flexibility in adjusting premiums and coverage.

What is Universal Life Insurance?

Universal life insurance is another permanent life insurance option that combines a death benefit with an investment component, offering greater flexibility than whole life insurance.

Key Features of Universal Life Insurance

- Flexible Premiums: Policyholders can adjust their premium payments within a specified range, allowing for financial flexibility.

- Adjustable Death Benefit: Some policies let you increase or decrease your coverage amount (subject to underwriting requirements).

- Investment Component: Your cash value is invested in market-based options, such as mutual funds or GICs, allowing for potentially higher returns.

- Tax-Advantaged Growth: Like whole life, the cash value grows tax-deferred, meaning you don’t pay taxes on gains until you withdraw funds.

- Loan and Withdrawal Options: You can access funds from the cash value, but withdrawals may reduce your death benefit and trigger tax liabilities.

Universal Life Insurance

Advantages:

- Flexibility in premium payments and coverage.

- Potential for higher cash value growth through investments.

- Control over investment choices.

Drawbacks:

- More complex and requires active management.

- Investment risk – returns are not guaranteed.

- Fluctuating premiums if cash value doesn’t perform well.

Key Differences Between Whole Life and Universal Life Insurance

| Feature | Whole Life Insurance | Universal Life Insurance |

|---|---|---|

| Premiums | Fixed for life | Flexible, can increase/decrease |

| Cash Value Growth | Guaranteed, stable | Variable, based on investments |

| Investment Options | Managed by insurer | Chosen by policyholder (stocks, bonds, GICs, etc.) |

| Death Benefit | Fixed amount | Adjustable in some cases |

| Risk Level | Low – predictable growth | Medium to High – depends on investments |

| Suitability | Best for those who want stable, long-term coverage with guaranteed growth | Best for those comfortable with market risk and need premium flexibility |

Which One is Right for You?

The choice between Whole Life Insurance and Universal Life Insurance depends on your financial goals, risk tolerance, and need for flexibility.

- Choose Whole Life Insurance if:

- You want a guaranteed death benefit and steady cash value growth.

- You prefer fixed premiums for predictable budgeting.

- You like a “set-it-and-forget-it” approach without managing investments.

- Choose Universal Life Insurance if:

- You want flexibility in premiums and coverage amounts.

- You are comfortable with investment risks and want higher growth potential.

- You want control over where your cash value is invested.

Final Thoughts

Both Whole Life Insurance and Universal Life Insurance provide lifelong coverage and a cash value component, but they cater to different financial needs. Whole life is ideal for those seeking stability and guaranteed benefits, while universal life offers flexibility and investment opportunities.

Before choosing a policy, consult with a licensed insurance advisor in Canada to tailor a plan that aligns with your financial situation and long-term goals.

Would you like a personalized quote or more details on specific insurers in Canada? Reach out to a financial professional today!

Leave a Reply